Will I Lose My House if I Need Nursing Home Care in Georgia?

Owning a home does not automatically mean you cannot qualify for Medicaid, but timing, transfer rules, and estate recovery matter.

For many Georgia families, the family home is one of the most emotionally and financially important assets they own. When long-term care becomes part of the conversation, one of the first questions families often ask is:

Will I lose my house if I need nursing home care?

The answer is not always simple. In many situations, owning a home does not automatically prevent someone from qualifying for Medicaid to help pay for nursing home care. However, the home may still be relevant when determining eligibility, and it may later be subject to Medicaid estate recovery after death.

Understanding the distinction between eligibility during life and estate recovery after death is essential.

Medicare, Medicaid, and Nursing Home Care

Before addressing the house specifically, it is important to understand the difference between Medicare and Medicaid.

Medicare may provide limited coverage for certain skilled nursing care after a qualifying hospital stay, but it generally does not pay for long-term custodial nursing home care.

Medicaid, by contrast, may help pay for long-term nursing home care for individuals who meet medical, income, and asset eligibility requirements. Because Medicaid is needs-based, eligibility involves careful review of income, assets, transfers, and other financial circumstances.

That is where the home often becomes a major concern.

Does Owning a Home Automatically Disqualify You from Medicaid?

Not necessarily. In Georgia, a primary residence, often referred to in Medicaid rules as the “homeplace,” may receive special treatment when determining Medicaid eligibility. Depending on the circumstances, a person may be able to own a home and still qualify for Medicaid long-term care benefits.

However, this does not mean the home is irrelevant. The treatment of the home can depend on factors such as:

Whether the home is the applicant’s primary residence

Whether the applicant intends to return home

Whether a spouse or certain family member continues to live in the home

The value of the home equity

Whether the home has been transferred

Whether the applicant is in a nursing facility long-term

Whether Medicaid estate recovery may apply later

This is why families should be cautious about assuming that the home is either fully protected or automatically lost.

Medicaid Eligibility and the Home During Life

For Medicaid eligibility purposes, the home may be treated differently from cash, investments, or other countable assets. A home may be excluded from countable resources in certain situations, particularly when it remains the person’s primary residence or when a spouse or certain family member continues to live there.

In practical terms, this means that a person may be able to qualify for Medicaid even while still owning a home, depending on the facts.

However, problems can arise when:

The home is vacant

The person does not intend to return home

No protected family member lives there

The home has significant equity

The home is transferred for less than fair market value

The home is sold and proceeds are retained

The family assumes the home is protected without understanding the rules

Medicaid rules are highly fact-specific. The same home may be treated differently depending on who lives there, how it is titled, whether it has been transferred, and whether the person applying for benefits is expected to return home.

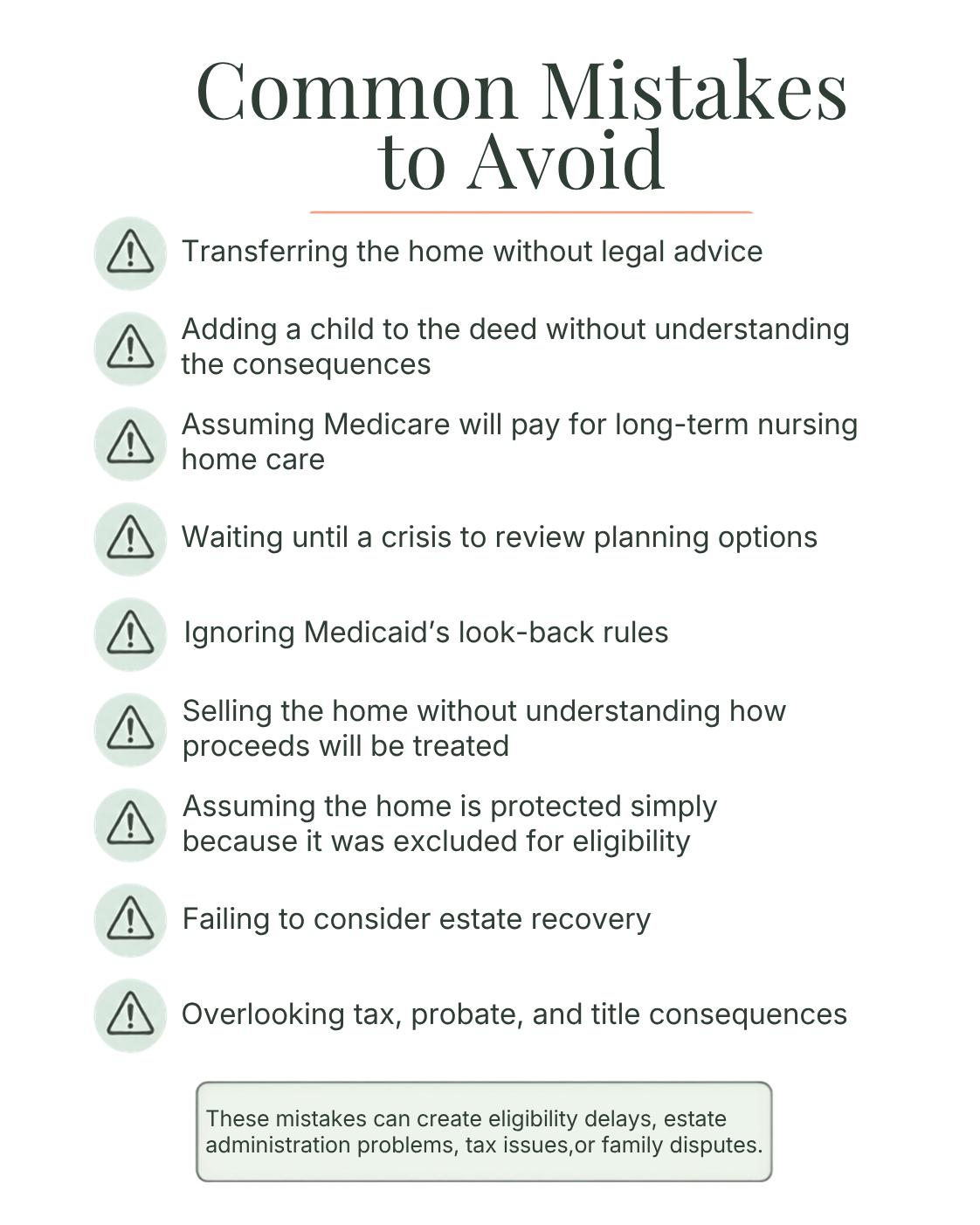

Can I Give the House to My Children Before Applying for Medicaid?

This is one of the most common and most risky misunderstandings.

Families sometimes assume that transferring a home to children will protect it from Medicaid. In reality, transfers made for less than fair market value can create Medicaid eligibility problems.

Georgia Medicaid generally reviews transfers during the applicable look-back period. If assets, including real estate, are given away or transferred for less than fair market value during that period, Medicaid may impose a penalty period during which benefits are delayed or denied.

This can create serious problems if nursing home care is needed before the penalty period is resolved.

Before transferring a home, adding someone to a deed, selling property for less than fair market value, or changing ownership, families should seek legal guidance. A well-intended transfer can create consequences that are difficult and expensive to correct later.

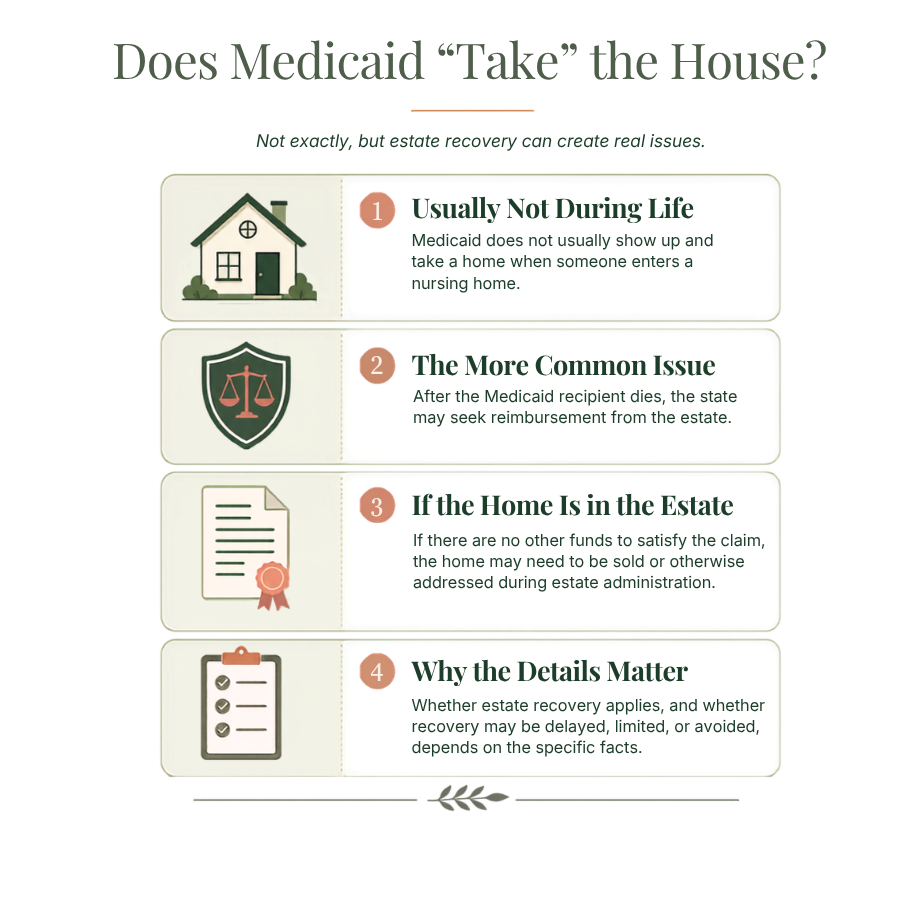

What Is Medicaid Estate Recovery?

Even if the home is not counted for eligibility during life, it may still be subject to Medicaid estate recovery after death.

Medicaid estate recovery is the process by which the state may seek reimbursement from a Medicaid recipient’s estate for certain benefits paid on that person’s behalf. In Georgia, estate recovery may apply to long-term care benefits, including nursing home care and certain home and community-based services.

This is the point many families miss:

The home may not prevent Medicaid eligibility during life, but it may still be at risk after death if it remains part of the estate.

Estate recovery often becomes an issue when the Medicaid recipient owned a home at death. Depending on the circumstances, the state may file a claim against the estate to recover amounts paid for care.

Concerned about a family home and future nursing home care? Conner Law Group helps Georgia families review estate planning, probate, Medicaid-related estate issues, and long-term care planning concerns before decisions are made in a crisis.

Schedule a consultation to discuss your family’s specific circumstances

What If a Spouse Still Lives in the Home?

A spouse continuing to live in the home can significantly affect the analysis.

Medicaid rules include certain protections for a spouse who remains in the community. These protections are designed to prevent the spouse at home from being left without basic support. If one spouse enters a nursing home and the other spouse remains at home, planning may involve issues such as:

Treatment of the residence

Income allocation

Resource limits

Community spouse protections

Estate recovery considerations after death

How assets are titled

This is one of the areas where early planning can make a meaningful difference.

What If an Adult Child or Family Member Lives in the Home?

A family member living in the home may also affect the planning analysis, depending on the relationship, circumstances, and applicable Medicaid rules. In some cases, the presence of certain family members may help preserve the home’s excluded status for eligibility purposes.

However, families should be cautious. Simply having a child or relative living in the home does not automatically mean the property is protected from Medicaid eligibility issues or estate recovery.

The facts matter, including:

Who lives in the home

How long they have lived there

Whether they are financially dependent on the home

Whether they provided care

Whether the home has been transferred

Whether the transfer was for fair market value

Whether documentation exists

Informal family arrangements can become difficult to prove later without proper documentation.

Planning Options Families May Consider

There is no one-size-fits-all solution. The right approach depends on the person’s health, age, family structure, assets, income, timing, and goals.

Planning may involve:

Reviewing how the home is titled

Evaluating whether estate planning documents are current

Considering whether a trust is appropriate

Coordinating beneficiary designations

Reviewing Medicaid eligibility rules before transfers are made

Evaluating potential estate recovery exposure

Preserving records of care, expenses, and property ownership

Planning for a spouse who remains at home

Addressing probate and title issues before a crisis occurs

The earlier a family begins planning, the more options may be available. Waiting until a nursing home admission is imminent often limits the available strategies.

How Estate Planning Can Help

Estate planning cannot guarantee that every long-term care issue will be avoided, but early planning can help you evaluate your options before a crisis occurs.

A coordinated estate plan may include:

A Will

A Revocable Living Trust, if appropriate

Durable Financial Power of Attorney

Advance Directive for Healthcare

Beneficiary designation review

Long-term care planning considerations

Special needs planning, where appropriate

Tax and fiduciary considerations

In many cases, the most important step is simply reviewing the plan before a crisis occurs. Documents that were prepared years ago may not reflect current family circumstances, property ownership, or long-term care concerns.

When Should Families Seek Guidance?

Families should consider seeking guidance if:

A loved one may need nursing home care

A family home is the primary asset

One spouse may remain at home

A parent wants to transfer property to children

There are concerns about Medicaid eligibility

A home may be sold to pay for care

There are questions about estate recovery

Family members disagree about what should happen to the house

Existing estate planning documents are outdated

Early guidance can help families understand what options exist before decisions are made that may be difficult to reverse.

Frequently Asked Questions

-

No. Owning a home does not automatically mean you will lose it or be disqualified from Medicaid. However, the home may affect eligibility depending on the facts, and it may later be subject to estate recovery after death.

-

Generally, no. Medicare may cover limited skilled nursing care in certain circumstances, but it does not generally pay for long-term custodial nursing home care.

-

Yes, in certain situations. Georgia Medicaid may seek recovery from a recipient’s estate for certain long-term care benefits paid on the recipient’s behalf.

-

Transferring a home can create Medicaid eligibility problems if done within the applicable look-back period or without proper planning. Families should seek legal guidance before transferring real estate.

-

Usually, yes. Planning earlier often provides more options and more flexibility. Crisis planning may still be possible in some situations, but waiting can limit available strategies.

Guidance for Georgia Families

The question “Will I lose my house if I need nursing home care?” does not have a simple yes or no answer. In Georgia, the family home may receive special treatment for Medicaid eligibility purposes, but it may still be affected by transfer rules, estate recovery, probate, and long-term care planning concerns.

Conner Law Group assists Georgia families with estate planning, probate, special needs planning, and tax-related matters that often intersect with long-term care concerns. If you are concerned about protecting a family home, planning for future care, or understanding Medicaid-related estate issues, thoughtful planning can help you evaluate your options before a crisis occurs.

Last reviewed: June 2026. Medicaid rules are fact-specific and may change, so families should seek advice based on their specific circumstances.