What Assets Count for Medicaid Eligibility in Georgia?

Understanding countable resources, exempt assets, and Medicaid planning for long-term care

When a loved one may need nursing home care or long-term care Medicaid in Georgia, one of the first questions families ask is:

What assets count for Medicaid eligibility?

The answer depends on the type of Medicaid being requested, the applicant’s marital status, how assets are titled, whether the applicant is seeking nursing home or waiver benefits, and whether any transfers were made before applying.

For Georgia families, this issue is especially important because Medicaid is a needs-based program. An applicant may medically need care, but still be denied or delayed if their countable assets are over the applicable resource limit.

This article focuses primarily on Georgia Medicaid eligibility for nursing home care and long-term care services.

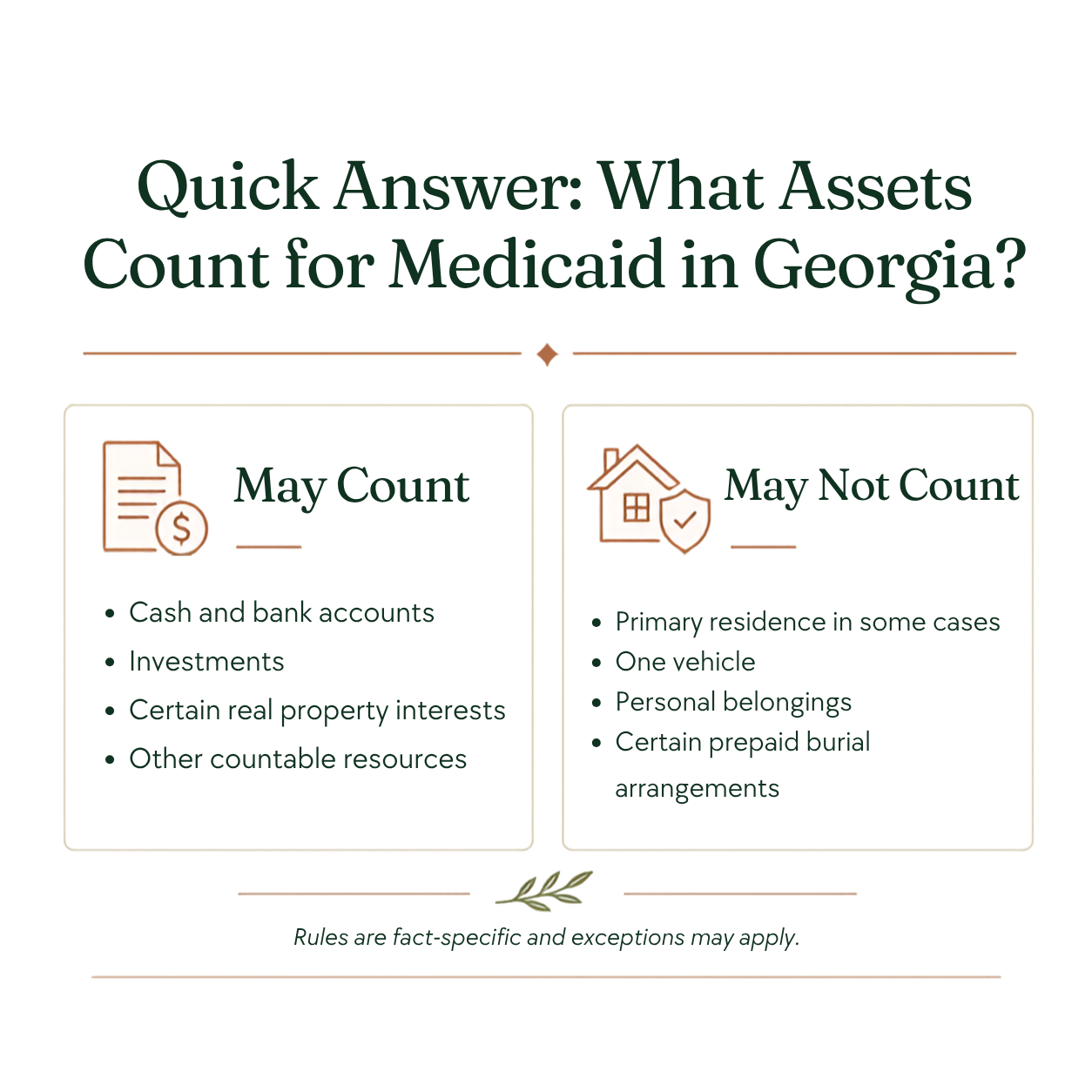

For long-term care Medicaid in Georgia, countable assets generally include resources that are available to the applicant and can be converted to cash.

These may include bank accounts, cash, investments, certain real estate, extra vehicles, some life insurance cash value, retirement accounts in some situations, and certain trust or annuity interests.

Some assets may be excluded, meaning they may not count toward the resource limit. Common excluded assets may include a primary residence in certain circumstances, one vehicle used for transportation, certain burial funds or prepaid burial arrangements, personal belongings, household goods, and assets protected for a community spouse.

The key issue is not simply what the applicant owns. The issue is whether Medicaid treats the asset as available and countable under the applicable program rules.

Medicaid Eligibility Is Not One-Size-Fits-All

Not every Medicaid category uses the same financial rules. Some Medicaid programs focus heavily on income. Others also apply a resource or asset test. Long-term care Medicaid, including nursing home Medicaid and certain home and community-based waiver programs, generally has both an income limit and a resource limit.

For many Georgia long-term care Medicaid applicants, the resource limit is very low. In 2026, the resource limit for nursing home Medicaid is generally:

Individual applicant: $2,000

Couple applying together: $3,000

For married couples where only one spouse needs long-term care, special spousal impoverishment rules may allow the spouse who remains at home to keep a protected amount of resources. This is called the Community Spouse Resource Allowance.

Because these numbers can change, families should verify the current limits before applying.

What Is a “Resource” for Medicaid Purposes?

Medicaid often uses the term “resource” instead of “asset.” A resource generally means something the applicant owns or has the legal right to access, use, sell, or convert to cash. If the applicant has ownership and legal access, Medicaid may treat the item as available unless a specific exclusion applies.

Common examples include:

Checking accounts

Savings accounts

Cash

Certificates of deposit

Money market accounts

Stocks

Bonds

Mutual funds

Non-home real estate

Extra vehicles

Cash surrender value of certain life insurance policies

Certain retirement accounts

Lawsuit settlements

Inheritances

Promissory notes or loans owed to the applicant

Some trusts or annuities

Jointly owned assets can also create eligibility issues. Families sometimes assume that if an account has another person’s name on it, only part of the account counts. That is not always true. Medicaid may look closely at ownership, access, contribution history, and whether the applicant can legally withdraw funds.

What Assets Usually Count for Georgia Medicaid?

The following assets commonly create Medicaid eligibility issues.

Bank Accounts

Checking and savings accounts are usually countable resources if the applicant owns or has access to them. This includes accounts held individually and may include jointly owned accounts.

Families should be careful with joint accounts. Adding a child to an account for convenience may create confusion about ownership. It can also raise transfer, tax, probate, or creditor issues.

Cash and Investments

Cash, stocks, bonds, mutual funds, CDs, and brokerage accounts are typically countable unless a specific exclusion applies. These assets are usually easy to value, so they are often reviewed closely during the application process.

Real Estate Other Than the Home

Real estate that is not the applicant’s primary residence is often countable. This may include:

A second home

Vacation property

Rental property

Land

Inherited property

A partial interest in real estate

A life estate or remainder interest

Property owned with siblings or other family members

The countable value is usually based on the applicant’s equity interest, not necessarily the full fair market value. However, co-owned property can still create significant eligibility and planning issues.

Extra Vehicles

Georgia Medicaid rules may exclude one vehicle used for transportation. Additional vehicles may be countable unless another exclusion applies. This can matter when an applicant owns multiple cars, an RV, a collectible vehicle, a farm truck, or a vehicle that is not actually used for the applicant’s transportation.

Life Insurance with Cash Value

Term life insurance generally does not have cash value. Whole life or other permanent life insurance may have cash surrender value. If a policy has cash surrender value, Medicaid may treat that cash value as a resource unless it fits within a specific exclusion. Burial-related exclusions may apply in some situations, but the rules are technical.

Families should not cancel, transfer, or borrow against life insurance without understanding the Medicaid consequences.

Retirement Accounts

Retirement accounts can be complicated. Depending on the type of account, ownership, payout status, accessibility, and applicable Medicaid category, a retirement account may be treated as a countable resource or may receive different treatment.

Examples include:

IRAs

401(k)s

403(b)s

Pensions

Annuities

Inherited retirement accounts

This is an area where families should get specific advice before applying, withdrawing funds, changing beneficiary designations, or moving assets.

Inheritances, Settlements, and Lump Sums

An inheritance, personal injury settlement, tax refund, insurance payment, or other lump sum may create Medicaid problems if it causes the applicant’s resources to exceed the limit.

A lump sum may also have different treatment in the month received compared to later months. If the funds remain available after the month of receipt, they may become a countable resource.

This is one reason it is important to seek advice quickly when a Medicaid recipient or applicant receives unexpected funds.

Trusts and Annuities

Trusts and annuities require careful review. Medicaid may consider who created the trust, whose assets funded it, whether distributions are available, whether the trust is revocable or irrevocable, and whether the trust complies with Medicaid rules.

Some trusts are useful Medicaid planning tools. Other trusts can create eligibility problems. A trust should not be assumed to protect assets simply because it is labeled “irrevocable.”

What Assets May Be Excluded for Medicaid Eligibility?

Some assets may be excluded, meaning they may not count toward the resource limit. Exemptions are fact-specific and should be reviewed carefully.

The Primary Residence

The home is often the most misunderstood Medicaid asset. A primary residence may be excluded for eligibility purposes in certain circumstances, including when the applicant, spouse, or certain dependent relatives live in the home, or when the applicant has an intent to return home. For institutionalized applicants, home equity limits and other special rules may apply.

This does not mean the home is permanently protected. Even if the home does not prevent Medicaid eligibility, it may still be exposed to Medicaid estate recovery after the Medicaid recipient’s death. Families should understand the difference between:

Eligibility during life

Estate recovery after death

The home may be excluded for one purpose but still create issues later.

One Vehicle

One vehicle used for transportation may be excluded. This can apply even when the applicant is in a nursing home, if the vehicle is used for the applicant or household transportation. Additional vehicles may count unless another exclusion applies.

Household Goods and Personal Effects

Ordinary household goods and personal belongings are generally not the assets that create Medicaid eligibility problems. Furniture, clothing, basic personal items, and ordinary household contents are usually treated differently from cash or investments.

High-value collectibles, valuable antiques, or unusual personal property should be reviewed separately.

Burial Funds and Prepaid Funeral Arrangements

Certain burial funds, prepaid funeral contracts, burial spaces, and related arrangements may be excluded if they meet Medicaid requirements.

The details matter. Whether the arrangement is revocable or irrevocable, whether funds are separately identified, whether life insurance is involved, and whether the amount exceeds the applicable exclusion can all affect eligibility.

Assets Protected for a Community Spouse

If one spouse needs nursing home care and the other spouse remains in the community, Medicaid does not necessarily require the couple to spend down to almost nothing.

The spouse at home may be entitled to keep a protected amount of countable resources under the Community Spouse Resource Allowance. The exact amount depends on the couple’s assets and the applicable Medicaid rules.

This is one of the most important planning areas for married couples. A Medicaid application should be coordinated carefully so that the community spouse is not left financially vulnerable.

Does Medicaid Count My Spouse’s Assets?

For married applicants, Medicaid may consider assets owned by either spouse, regardless of whose name is on the account or property. However, spousal impoverishment rules may allow the spouse who remains at home to keep certain income and resources.

This is different from the common assumption that separate accounts are automatically separate for Medicaid purposes.

For example, an account titled only in the community spouse’s name may still need to be disclosed and reviewed. At the same time, the community spouse may be allowed to keep a protected share of the couple’s countable assets.

The timing of the application, the snapshot of assets, and the spend-down strategy can all matter.

Does My House Count for Medicaid in Georgia?

Sometimes yes, sometimes no. For eligibility purposes, the home may be excluded if it qualifies as the applicant’s home and the applicable conditions are met. If the applicant is in a nursing home, the home may still be excluded if the applicant retains ownership and meets the applicable equity and intent rules, or if certain family members live in the home.

However, the home can still matter after death because of Medicaid estate recovery. This is where families often get confused. Medicaid may not force the sale of the home before approving benefits, but that does not mean the home is immune from later claims.

Does Medicaid “Take” the House?

Medicaid does not usually come in and take the house when someone enters a nursing home. The more common issue is estate recovery. After a Medicaid recipient dies, Georgia may seek reimbursement from the recipient’s estate for certain Medicaid benefits paid, including long-term care services. Estate recovery can affect real property, probate administration, heirs, and title issues. There are exceptions, delays, hardship waivers, and special rules, but families should not assume the house is protected simply because it did not count for eligibility. For more in depth information, please see our previous post on the subject, here.

Can I Give Assets Away to Qualify for Medicaid?

This is one of the biggest Medicaid planning mistakes. Transfers for less than fair market value can create a Medicaid penalty period. This can include gifts to children, transfers of real estate, adding someone to a deed, moving funds out of an account, or selling property for less than it is worth.

For long-term care Medicaid, Medicaid generally reviews transfers made during the look-back period before the application. If transfers are found, the applicant may be medically and financially eligible but still be denied payment for nursing home care for a period of time. Before transferring assets, families should get legal advice. A well-intended transfer can create a serious eligibility problem.

What About Spending Down Assets?

Spend-down does not mean giving everything away. It generally means using countable assets in a permissible way so that the applicant reaches the Medicaid resource limit without creating a transfer penalty.

Possible spend-down options may include:

Paying legitimate debts

Paying for care

Making home repairs or accessibility improvements

Purchasing medical equipment

Buying personal items for the applicant

Prepaying certain funeral or burial expenses

Replacing an older vehicle

Paying legal fees for Medicaid or estate planning advice

The right spend-down plan depends on the applicant’s assets, health, marital status, timing, and goals.

Families should keep receipts and documentation for all spend-down transactions.

Common Mistakes Families Make

Families often run into trouble because they act before getting advice.

Common Medicaid asset mistakes include:

Transferring the home to children without understanding the look-back rules

Adding a child to a deed or bank account without legal advice

Giving away money shortly before applying

Selling property for less than fair market value

Failing to report jointly owned accounts

Assuming the home is fully protected

Ignoring estate recovery

Cashing out life insurance or retirement accounts without advice

Using a generic trust that does not comply with Medicaid rules

Waiting until a crisis to review planning options

These mistakes can cause eligibility delays, penalty periods, tax problems, probate issues, and family disputes.

What Documents Are Needed to Review Medicaid Assets?

Before applying for Georgia long-term care Medicaid, families should gather financial records.

Helpful documents include:

Bank statements

Investment account statements

Retirement account statements

Life insurance policies

Deeds and property tax records

Vehicle titles and registrations

Prepaid funeral or burial contracts

Trust documents

Annuity contracts

Promissory notes or loan documents

Records of gifts or transfers

Prior tax returns

Marriage certificate

Power of attorney

Health care directive

Recent care facility bills

The more complete the records, the easier it is to identify eligibility issues before the application is filed.

Medicaid Asset Rules and Estate Planning Should Work Together

Medicaid planning should not be separated from estate planning.

A power of attorney may determine who has authority to access records, sign applications, manage assets, or complete a lawful spend-down. A will or trust may affect what happens to the home after death. Beneficiary designations may affect whether assets pass through probate. Special needs planning may be needed if a beneficiary receives SSI or Medicaid.

For many Georgia families, the best plan considers:

Medicaid eligibility

Estate recovery

Real estate title

Care needs

Family relationships

Powers of attorney and decision-making authority

A plan that solves only one issue may create problems elsewhere.

Common Questions About Medicaid Assets in Georgia.

-

For 2026, the general resource limit for an individual applying for Georgia nursing home Medicaid is $2,000. For a couple applying together, the general resource limit is $3,000. Married couples where only one spouse applies may have additional protections under spousal impoverishment rules.

-

The home may be excluded in certain circumstances, especially if it is the applicant’s primary residence, the applicant intends to return home, or a spouse or certain dependent relatives live there. However, the home may still be subject to estate recovery after death.

-

Retirement accounts can be complicated. Whether an IRA, 401(k), pension, or annuity counts may depend on the type of account, payout status, accessibility, ownership, and Medicaid category.

-

One vehicle, used for transportation, may be excluded. Additional vehicles may count unless another Medicaid exclusion applies.

-

Certain burial funds, prepaid funeral contracts, and burial spaces may be allowed if properly structured. The details matter, so these should be reviewed before purchase or designation.

-

Giving away money or property can create a Medicaid transfer penalty. Families should not transfer assets without understanding the look-back period and penalty rules.

-

No. Medicaid rules distinguish between countable resources, excluded resources, income, spousal protections, and estate recovery. However, the resource limits are strict, and planning should be done carefully.

-

No, but they overlap. Medicaid planning focuses on eligibility and payment for care. Estate planning addresses decision-making authority, asset distribution, probate, trusts, tax issues, and family protection. A good plan should consider both.

Final Thoughts

For Georgia Medicaid eligibility, the question is not simply “What do I own?” The better question is:

Which assets are countable, which assets are excluded, and what planning options are available before applying?

Bank accounts, investments, non-home real estate, extra vehicles, cash value life insurance, retirement accounts, inheritances, and certain trusts may all affect eligibility. The home, one vehicle, burial arrangements, personal property, and spousal protections may receive special treatment, but only if the rules are satisfied.

Families should be cautious before transferring property, spending down assets, or applying without a full review.

Conner Law Group helps Georgia families understand estate planning, probate, guardianship, special needs planning, and Medicaid-related planning issues. If your family is trying to understand what assets may count for Medicaid eligibility in Georgia, it may be time to review your options before a crisis develops.